PUBLIC FINANCE MANAGEMENT ACT: INDEX TO SUBSIDIARY LEGISLATION

Finance (Control and Management) (Public Stores) Regulations

Public Finance Management (General) Regulations

FINANCIAL REGULATIONS

[Section 18]

[RETAINED AS PER S.15 OF INTERPRETATION AND GENERAL PROVISIONS ACT]

Arrangement of Regulations

Regulation

PART I

PRELIMINARY

1. Title

2. Effective date

3. Interpretation

4. Regulations

PART II

AUTHORITIES FOR EXPENDITURE

5. Available funds authorities

PART III

ESTIMATES PROCEDURE

6. Form of estimates

7. Draft estimates

8. Presentation of estimates to National Assembly

9. Appropriation Act

10. Treasury Authorities

11. Provisional Warrant

12. Finance circular of authority (provisional)

13. Treasury Authority

14. Procedure if provision inadequate

15. Supplementary expenditure

16. Transfer of savings

17. Supplementary estimates

18. Copies to Auditor-General

19. Restrictions on expenditure

20. Annual recurrent authorities

21. Capital estimates

PART IV

GENERAL ACCOUNTING RESPONSIBILITIES

22. Accounting units

23. Returns and reports

24. Inspections

25. Responsibilities of controlling officers

26. Reports by accounting officers

27. Claims of questionable validity

28. Responsibilities of accounting officers

29. Erasures in accounts

30. Mutilated currency

31. Register of cheques and cash

32. Approval of accounting systems and forms

33. Observance of orders by controlling officers

34. Delegation of responsibility

35. Audit queries

36. Below-the-line accounts

37. Balancing of below-the-line accounts

38. Banking of cheques and cash

39. Reconciliation of bank accounts

40. Checking of cash

41. Checking of computer documents

42. Dates and times of submission of computer documents

43. Payments at end of financial year

44. Procedure at end of financial year

45. Public Accounts Committee

46. Memoranda for Public Accounts Committee

47. Internal audit

48. Controlling officers not relieved of responsibility

49. Responsibilities of internal auditors

50. Reports by internal auditors

51. Preservation of accounting records

PART V

SAFES, STRONG BOXES, CASH BOXES AND SPECIE BOXES

52. Definition of “safes”

53. Responsibility for obtaining safes

54. Care of safes

55. Responsibility for keys

56. Duplicate keys

57. Handing over of keys prohibited

58. Original keys

59. Control over duplicate keys

60. Inspection reports

61. Transfer within Ministries

62. Transfer between Ministries

63. Loss of keys

64. Private moneys in public safes

65. Register

66. Weekly check

67. Cash in transit

PART VI

BANK ACCOUNTS AND CHEQUES

68. Bank accounts and bank signing arrangements

69. Instructions to banks

70. Use of public money

71. Cheque forms

72. Security of unused cheques

73. Lost cheques

74. Signing of cheques

75. Overdraft

76. Acceptance of cheques

77. Security of cheques received

78. Dishonoured cheques

79. Cancellation of licences

80. Cheques on accounts outside Zambia

81. Cashing of Government cheques

82. Bank statements

83. Audit of cheques

84. Security of cheques in payment for goods supplied on Local Purchase Orders

PART VII

RECEIPT FORMS

85. Definition of “receipt form”

86. Issue of receipts

87. Obtaining receipt forms

88. Auditor-General to be informed

89. Checking receipts received

90. Register of receipt forms

91. Transfer of receipts

92. Consecutive issues

93. Unused and surplus receipts

94. Destruction of obsolete receipts

95. Recording of destruction of obsolete forms

96. Reporting of loss of or damage to receipt forms

97. Monthly check of unused receipt forms

98. Handing over certificates to record receipt forms

99. Notice to public about official receipts

100. Completion of receipts

101. Cancelled receipts

102. Method of cancelling receipts

103. Office of issue of receipts

104. Consecutive receipts

105. Free issue of receipt form

106. Duplicate licences

107. Certified copies of receipt forms

108. Transfer and destruction of receipt forms

PART VIII RECEIPT OF REVENUE

109. Private use of revenue prohibited

110. Receipts to be issued

111. Receipt forms

112. Legal tender

113. Foreign currencies

114. Remittance of foreign currency

115. Classification of revenue

116. Cash books

117. Bringing revenue to account

118. Deposits to the Main Account

119. Cash surplus

120. Revenue collectors not to open mail

121. Recovery of overpayments

122. Revenue not to be credited to suspense account

123. Abandoned revenue

PART IX

REFUNDS OF REVENUE

124. Authority for refunds

125. Refunds of stamp duty

126. Vouchers for refunds

127. Court fees and fines

128. Classification of refunds

PART X

CONTROL OF EXPENDITURE AND PAYMENTS

129. Authorities by warrant

130. Authorities on vouchers

131. Record of commitments

132. Payments on behalf of other Ministries

133. Date of payment

134. Payment vouchers

135. Details on payment vouchers

136. Preparation of vouchers

137. Signing of vouchers

138. Panel of signing officers

139. Responsibilities of officers signing vouchers

140. Recoverable payments

141. Suppliers’ invoices to be attached

142. Mislaid invoices

143. Mislaid requisition forms

144. Payments on incorrect certificates

145. Payees outside Zambia

146. Methods of payment

147. Security of open cheques

148. Periodic payments

149. Responsibilities of cheque signatories

150. Delivery of cash or cheques

151. Identification of payees

152. Daily accounting for payments

153. Issue of travel warrants

154. Responsibility of officers signing warrants, etc.

155. Extraordinary payments

156. Custody of original documents

157. Loss of payment vouchers

PART XI

PAYMENT OF SALARIES AND WAGES

158. Day of payment

159. Calculation of salary

160. Salaries and wages not to be paid in advance

161. Adjustment of salary or other moneys due to death, etc.

162. Salaries of convicted officers

163. Method of payment and deductions: Divisions I and II

164. Method of payment

165. Dispatch of salary cheques

166. Deduction of rent for official quarters

167. Payment scales and rates: officers other than those in Divisions I and II

168. Gross salary and deductions to be charged

169. Salary records

170. Unclaimed wages

171. Security precautions with regard to payment of wages

172. Leave salary

173. Attendance records

PART XII

IMPRESTS

174. Types of imprest

175. Special imprests outside Zambia

176. Authority to issue imprests

177. Sub-imprests

178. Amount of standing imprest

179. Amount of special imprest

180. Special imprests: limitation

181. Restriction in use of imprests

182. Register of Imprests

183. Banking of imprests

184. Field Cash Book

185. Reimbursement of standing imprests

186. Retirement of special imprests

187. Retirement of standing imprests

PART XIII

HANDLING AND TAKING OVER

188. Handing-over procedure

189. Safe keys

190. Discrepancies on handing over

191. Handing-over certificate

PART XIV

LOSSES OF PUBLIC MONEY AND STORES

192. Definition of “losses”

193. Investigation of loss

194. Write-off by controlling officer

195. Report by controlling officer

196. Write-off by Secretary to the Treasury

197. Assessment of claim against defaulting officer

198. Representations by officer

199. Decision of Secretary to the Treasury

200. Admission of liability

201. Failure to admit liability

202. Monthly deductions

203. Officers leaving the service

204. Statement to Attorney-General

PART XV

REMITTANCES OF CASH

205. Remittances to a bank or other office

206. Remittances received

PART XVI

SI 398 of 1969,

SI 156 of 1971,

SI 186 of 1979,

SI 97 of 1987,

SI 69 of 1990,

SI 36 of 1991,

SI 102 of 1991.

[Regulations by the Minister]

PART I

PRELIMINARY

These Regulations may be cited as the Financial Regulations.

These Regulations come into operation on the 12th September, 1969.

In these Regulations, unless the context otherwise requires—

“accounting officer” means any officer or other person concerned with the collection, receipt, custody, issue or payment of public or other moneys, stores, stamps, investments, securities or negotiable instruments, whether the property of the Republic or entrusted to the Republic or to any officer in his capacity either alone or jointly with any other officer;

“accounting unit” means a section established on the authority of the Secretary to the Treasury to maintain the accounts of a Ministry or of a number of Ministries or a branch of a Ministry which has an official designated in the estimates of expenditure as a controlling officer;

“advance” means any recoverable sum of money issued to any person where such advance is in the public interest and is repayable at some future date;

“below-the-line accounts” means suspense accounts which include advances, deposits, imprests, remittances and special funds;

“collector of revenue” means any officer charged, temporarily or permanently, with the duty of collecting any type of Government revenue;

“controlling officer” means an officer designated by the Minister as officer in charge of a head of expenditure in any one financial year and charged with the duty of controlling expenditure on any public service under that head;

“internal auditor” means any person designated as such by the Secretary to the Treasury;

“Ministry” means the Ministry of Finance;

“personal emoluments” means the salaries and allowances of all monthly paid civil servants and members of the Teaching Service.

These Regulations and such subsequent regulations as may be issued from time to time under the authority of the Act supersede previous Financial Orders and Financial Regulations.

PART II

AUTHORITIES FOR EXPENDITURE

5. Available funds authorities

A controlling officer may not cause or permit any expenditure to be incurred, unless funds are available under one or more of the following authorities—

(a) The issue of a circular by the Secretary to the Treasury to the effect that a Provisional Warrant has been signed by the President.

(b) A Treasury Authority (Recurrent Expenditure) (Finance Form 5) issued by the Secretary to the Treasury when the General Warrant has been signed.

(c) A Treasury Authority (General) (Finance Form 4) issued by the Secretary to the Treasury conveying authority for the transfer of funds between items or for the provision of additional funds for a sub-head/item.

(d) A Treasury Authority (Establishments) (Finance Form 13) issued by the Secretary to the Treasury in respect of variations in posts or provisions in the “personal emoluments” sub-head.

(e) An approved Capital Expenditure Requisition (Finance Form 1) signed by the Secretary to the Treasury.

PART III

ESTIMATES: PROCEDURE

The estimates of capital and recurrent expenditure laid before the National Assembly in accordance with the provisions of the Constitution shall be set out as follows—

(a) The total expenditure shall be shown under the head of expenditure in respect of which a controlling officer shall be designated.

(b) Under each head of expenditure there shall be shown sub-heads.

(c) The first sub-head under each head of recurrent expenditure shall be the estimated expenditure on personal emoluments in respect of such head of expenditure and there shall be annexed to the estimates a supporting document entitled an “Establishment Register” which shall be deemed to be part of the estimates and which shall show, in respect of each head of expenditure, the grades and salary scales of the posts included in the sub-head for personal emoluments.

(d) Except in the case of the sub-head “personal emoluments”, there shall be shown items of expenditure in respect of each sub-head of recurrent expenditure.

The submission of draft recurrent estimates will be called for in an annual estimates circular issued by the Secretary to the Treasury. Controlling officers will frame their draft estimates in the form in which they are to be rendered, including supporting schedules and other details required in the circular.

8. Presentation of estimates to National Assembly

The draft estimates will be examined in the Ministry and, where necessary, amendments will be made before the estimates are laid before the National Assembly by the Minister.

Following the passing of the Appropriation Act under section 109(2) of the Constitution and the issue of the General Warrant by the President, expenditure shall be limited to the amounts included in the approved estimates.

Treasury Authorities for expenditure will be issued by the Secretary to the Treasury.

Under Article the Constitution, the President may issue a Provisional Warrant to cover expenditure necessary to carry on the services of the Government for any period, not exceeding four months beginning at the commencement of a financial year, before the Appropriation Act for that financial year is passed. This warrant will authorise payment of all personal emoluments, pensions and other charges which become due in respect of expenditure for existing establishments, of inescapable, recurrent commitments and any other items which are specifically defined in the Treasury Authorities. No other expenditure may be incurred outside these limitations. Furniture, stores, vehicles or equipment of any kind will not be bought, nor will new posts be filled until the Secretary to the Treasury has issued a Treasury Authority to controlling officers, even if provision for these services and purchases has been included in the estimates.

12. Finance circular of authority (provisional)

The fact that the Provisional Warrant has been signed will be conveyed to controlling officers by a circular issued by the Secretary to the Treasury. This circular will constitute the authority for controlling officers to incur or permit expenditure within the limitations in regulation 11.

On receiving the General Warrant from the President, the Secretary to the Treasury will, by the issue of a Treasury Authority (recurrent expenditure), authorise controlling officers to incur and commit expenditure during the current financial year within the amounts set out in the estimates for that year.

14. Procedure if provision inadequate

The Appropriation Act authorises expenditure under separate main heads, but payments will be allocated to the individual sub-heads and items shown in the printed estimates. Should it become apparent that the provision is inadequate, action must be taken in accordance with regulations 15, 16 and 17.

When the expenditure is of a nature which was not envisaged when the estimates were prepared, or when the excess expenditure on an item cannot be met from savings on another item under the same sub-head, the controlling officer will submit to the Secretary to the Treasury an application for Supplementary Provision, together with a Treasury Authority (General) completed at Part 2. This application will show savings from any other sub-head under the same head, or evidence that the additional expenditure will result in a corresponding increase in revenue.

If the excess expenditure on one item can be met from savings on another item within the same sub-head, an application for Treasury Authority will be submitted for approval to the Secretary to the Treasury.

Applications for Supplementary Provision which have the support of the Secretary to the Treasury will be submitted by him to the National Assembly in accordance with the Constitution. When the National Assembly has approved the Supplementary Provision and a Warrant has been signed by the President, the Secretary to the Treasury will issue an appropriate Treasury Authority to the controlling officer concerned.

The Secretary to the Treasury shall send copies to the Auditor-General of all Supplementary Provision Warrants and Treasury Authorities immediately after authorisation.

19. Restrictions on expenditure

The Secretary to the Treasury may impose a restriction on expenditure under any sub-head or item appearing in the estimates. The controlling officer will be informed of the reason for the restriction and the circumstances under which he can apply to have the restriction removed or varied. Approval for complete or partial removal of a restriction will be conveyed by the issue of a revised Treasury Authority (recurrent) by the Secretary to the Treasury.

20. Annual recurrent authorities

All authorities to incur expenditure under the recurrent estimates expire on the last business day of the financial year to which they refer. No payment may be made against these authorities after that date.

Instructions regarding the capital estimates will be issued from time to time by the Secretary to the Treasury.

PART IV

GENERAL ACCOUNTING RESPONSIBILITIES

Each accounting unit shall be under the control of the controlling officer.

Controlling officers shall submit from time to time such returns and reports, as may be required by the Secretary to the Treasury, of revenue collected by them or funds expended under a head for which they are responsible. This will include “below-the-line accounts” under their control.

Controlling officers will make arrangements for periodic checks of cash and stamps held by accounting units or branches thereof under their control. These checks should be carried out at irregular intervals and as frequently as possible, preferably at least four times a year. Checking officers will be required to sign legibly at the point of check in the cash book or register covering the check.

25. Responsibilities of controlling officers

The controlling officer shall be responsible for keeping accounts in accordance with any order issued or approved by the Secretary to the Treasury; for the accuracy of these accounts and for the safe custody of all public money entrusted to him. He shall ensure that officers accounting for revenue and expenditure for which he is responsible, comply with these Regulations and any supplementary instructions issued by him pursuant to these Regulations.

26. Reports by accounting officers

Accounting officers shall be responsible for—

(a) reporting to the controlling officer if it appears that any head, sub-head or item is likely to be overspent;

(b) drawing the attention of the controlling officer to delays and shortages in the collection of revenue, for which the controlling officer is responsible; to any advance or imprest account which they are unable to clear at the time that it should be cleared; to any deposit account which has become dormant and to any weakness in the accounting system employed, or in the internal checks applied to accounting transactions.

27. Claims of questionable validity

Accounting officers shall refer to their controlling officers any claim of an unusual nature, or any claim the validity of which is doubtful and any claim in respect of expenditure which, in their opinion, is not provided for in the approved estimates. In the event of an accounting officer receiving instructions to make a payment which he is not satisfied is covered by a financial authority, he shall state his objection in writing to his controlling officer:

Provided that, if an instruction is then given in writing by the controlling officer, a payment may be made or accepted, and responsibility for the payment then rests with the controlling officer, who will be held personally liable. After making the payment, the accounting officer shall inform the Auditor-General and the Secretary to the Treasury of the circumstances.

28. Responsibilities of accounting officers

The responsibilities of an accounting officer shall be—

(a) to account for receipts and disbursements of public money in accordance with these Regulations;

(b) to see that proper arrangements are made for the safekeeping of public moneys, securities, stamps, stamp dies, revenue counterfoil receipts, licences, warrants and all forms of requisition;

(c) to collect punctually all revenue and other public money which it is his duty to collect;

(d) to bring to account promptly under the correct head and sub-head all public money which he collects or which is paid to him;

(e) to check regularly all cash and stamps in his charge and to verify the amounts with the balances shown in the cash book or stamp register;

(f) to bring to account promptly any revenue in cash or stamps found in his charge in excess of the balances shown in the cash book or stamp register;

(g) to make good any shortage in cash or stamps for which he is responsible;

(h) to ensure that all disbursements made or incurred by the issue of payment vouchers, orders, warrants, requisitions or any other documents are properly authorised;

(i) to charge in the accounts under the proper head or accounting allocation all expenditure when it occurs;

(j) to ensure the satisfactory control of the funds warranted to him by maintaining a record of commitments incurred by his controlling officer;

(k) to prepare and dispatch promptly all financial statements and returns in the form and manner prescribed;

(l) to see that his books of account are correctly posted and kept up to date;

(m) to report in writing to his controlling officer any apparent defect in the procedure of revenue collection, any apparent waste and any extravagance in expenditure which comes to his notice in the course of his accounting duties;

(n) to produce when required by the Secretary to the Treasury, or by the Auditor-General, all books and records or accounting documents in his charge;

(o) to reply promptly and fully to any observations or queries received from the Auditor-General, from the Secretary to the Treasury or from his controlling officer;

(p) to exercise strict supervision over all officers under his authority, and by the maintenance of efficient checks to take precautions against fraud and nugatory expenditure;

(q) to bring to the notice of his controlling officer any incompetence, carelessness or insubordination on the part of his staff;

(r) to study the convenience of the public and institute such arrangements as may be properly made to facilitate the transaction of business with the public.

No erasures may be made in accounts. Corrections must be made by striking out the incorrect figures and writing the correct figures above them. The corrections must be made in such a way that the original figures are still legible. Corrections must be initialled by the officer who makes them. On no account may alterations be made to figures which have already been audited.

Accounting officers should not accept mutilated Zambian currency, but they may assist the public by informing them where to obtain a replacement of any mutilated currency of which they are the Lawful owners. Mutilated notes and coins can be replaced on application to the Bank of Zambia. An “Application for Replacement of Mutilated Currency” Form (obtainable from local banks) should be sent with the mutilated currency to the General Manager, Bank of Zambia, P.O. Box 80, Lusaka.

31. Register of cheques and cash

Officers responsible for dealing with incoming mail which contains money shall keep a Register of Cheques and Cash (Accounts Form 61A) for the purpose of recording details of remittances received.

32. Approval of accounting systems and forms

(1) The procedures and systems, including the use and introduction of forms, adopted by Ministries for controlling their expenditure shall be subject to the prior approval of the Secretary to the Treasury. Each accounting unit will keep such books of account as are prescribed from time to time by the Secretary to the Treasury.

(2) A register of all official accounting documents will be kept by the Secretary to the Treasury.

33. Observance of orders by controlling officers

Controlling officers are personally responsible for the observance of all instructions issued by the Secretary to the Treasury.

34. Delegation of responsibility

When it is necessary for any officer to delegate to another officer any financial duty for which he is responsible, he will ensure that the delegation, its scope and duration, is in clear and specific terms.

All observations or queries raised by the Auditor-General must be answered promptly and fully.

With the approval of the Secretary to the Treasury, controlling officers may operate such “below-the-line accounts” as are necessary for the efficient management of the financial operations under their control. “Below-the-line accounts” will not be used, in any circumstances, for receipts and payments which can properly be allocated to revenue or expenditure in the first place, nor will they be used for holding amounts charged to recurrent expenditure in one year for subsequent payment in the next financial year.

37. Balancing of below-the-line accounts

The balancing and reconciliation of “below-the-line accounts” must be carried out, and all outstanding items cleared, at the end of each month.

38. Banking of cheques and cash

All cheques and cash received will be banked not later than the business day following the day of receipt. In no circumstances will funds be allowed to accumulate in accounting units.

39. Reconciliation of bank accounts

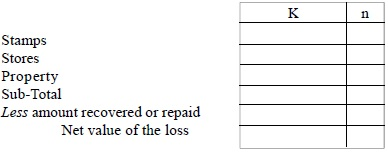

Controlling officers will forward to the Secretary to the Treasury within 14 days of the end of each month the following form of reconciliation:

|

K |

n |

|

| Cheques outstanding for the previous month | ||

| Add cheques drawn during the month | ||

| Sub-total | ||

| Less cheques presented during the month | ||

| Cheques outstanding at the end of the month |

The total of cheques outstanding at the end of the month must agree with the total of the schedule of unpresented cheques attached to this reconciliation. The date of issue and the number and amount of each unpresented cheque will be shown.

Controlling officers will check, not less than once monthly, any cash held by their accounting units and will ensure that the cash balance is at all times correct. Personal cheques which are cashed from an imprest will be redeemed for cash or credited to the Imprest Banking Account on the first banking day after the cashing of the cheque. Post-dated cheques will not be accepted.

41. Checking of computer documents

(1) Documents will be submitted by each accounting unit for computer processing in the manner prescribed from time to time by the Secretary to the Treasury. Only documents required for punching purposes will be submitted. Supporting documents not intended for punching will be retained by the originating accounting unit.

(2) A register will be kept by each accounting unit of all documents submitted to and returned by the Data Processing Unit in the Ministry, showing the dates and times of dispatch and receipt of documents.

42. Dates and times of submission of computer documents

Dates and times of submission of documents will be laid down from time to time by the Secretary to the Treasury. These dates and times must be strictly adhered to and must not be altered except with the approval of the Secretary to the Treasury.

43. Payments at end of financial year

(1) All accounts received before the last day of the financial year must, as far as possible, be paid before the accounts are closed. This means that, where reimbursements are required from other accounting units or other organisations, they will be notified in time to permit those organisations to make payment before the end of the financial year. Similarly, all moneys received before the end of the financial year must be brought to account before the accounts are closed.

(2) Special arrangements will be made by the Secretary to the Treasury to ensure that transactions appearing in Agents’ Accounts are notified to accounting units up to the latest possible date that will enable the transactions in the last month of the financial year to be charged to the correct votes before the accounts are closed.

(3) The Stores Department will normally close its accounts with accounting units on the 14th December and will send out invoices accompanied by a statement up to the closing date. These invoices will be charged against Ministerial suspense accounts and will be cleared by accounting units against expenditure votes before the closing of the main accounts for the financial year.

(4) Requisitions held by the Stores Department which cannot be filled before the date of closing of the Stores Accounts will be a first charge against the accounts of requisitioning Ministries in the following financial year.

44. Procedure at end of financial year

The procedures to be followed by accounting units at the close of the financial year are set out hereunder. It will be the responsibility of the controlling officer to see that action called for is taken at the appropriate times and that returns are submitted within the stated periods—

(a) At the close of business on the last day of the financial year, all cash books will be ruled off, signed and dated by the responsible officers.

(b) The accounts will be closed in the normal manner, as for an ordinary month end, but supplementary accounts will be opened by accounting units only for the purpose of adjusting misallocations, for the transfer of revenue and/or expenditure to other accounting units and for final entries on the closing of the accounts.

(c) Any revenue or expenditure (recurrent or capital) which appears in the accounts of one accounting unit but which is controlled by another, will be transferred. Only revenue and expenditure actually controlled by an accounting unit will appear in the accounts of that unit for clearance to the “Surplus and Deficit Account” maintained in the books of the Ministry under the procedure described in paragraph (g).

(d) Dummy codes will not be used in any circumstances or for any reason.

(e) Should the recoveries under items of “Appropriations-in-Aid” be in excess of the approved estimate for the year, the amount of the excess will be credited to the revenue item “Excess Appropriations-in-Aid”.

(f) The final closing of the accounts will be made not later than one month after the last day of the financial year.

(g) Immediately after the final closing of the accounts, accounting units will transfer all items of Recurrent and Capital Revenue and Expenditure to the “Surplus and Deficit Account” in the books of the Ministry. The final control balance for each unit will reflect only the balances outstanding on “below-the-line accounts”.

(h) Within two months of the end of the financial year, statements of revenue and expenditure and “below-the-line accounts”, together with balance sheets and accounts of all funds, will be submitted in quadruplicate by all accounting units to the Ministry for inclusion in the Financial Report. All statements, balance sheets and accounts will be signed personally by controlling officers. A circular minute detailing special requirements will be issued by the Secretary to the Treasury.

Controlling officers may be required to submit to the Public Accounts Committee memoranda on subjects which concern their Ministries and which are mentioned in the Report of the Auditor-General on the accounts for the preceding year.

46. Memoranda for Public Accounts Committee

Controlling officers who are required to submit memoranda to the Public Accounts Committee will ensure that these memoranda reach the Clerk of the National Assembly 14 days before the notified date on which the Public Accounts Committee is to sit. The following form of memorandum will be used, and controlling officers will personally sign all such memoranda:

PUBLIC ACCOUNTS COMMITTEE

Report of the Auditor-General on the Public Accounts for the year ended …………….., 20 ……..

(memorandum by the Controlling Officer, Ministry of……………………………….)

Paragraph No.* ………………… Subject ……………………….

……………………………. Body of Memorandum Date ………………………

………………………….. Controlling Officer

*This refers to the appropriate paragraph in the Auditor-General’s Report.

Twenty copies of each memorandum will be sent to the Clerk of the National Assembly who will be responsible for forwarding copies to the Secretary to the Treasury and the Auditor-General.

Internal audit teams will be provided for specified accounting units by the Secretary to the Treasury.

48. Controlling officers not relieved of responsibility

The existence of internal audit teams will not relieve controlling officers or any other accounting officers of their individual responsibilities, nor will it remove the need for normal checks within Ministries or Departments.

49. Responsibilities of internal auditors

Internal auditors will be directly responsible to the controlling officers of the Ministries in which they are provided. The programme of checks to be carried out by internal auditors will be laid down by the Secretary to the Treasury in consultation with controlling officers and with the Auditor-General, and will cover all accounting procedures and documentation. Generally, internal auditors will ensure—

(a) that the work entailed in the receipt and payment of public money has been properly carried out under proper supervision;

(b) that the safeguards for the prevention or prompt detection of fraud or loss of stores, cash or other Government assets, are adequate;

(c) that accounting forms are properly protected, recorded and regularly checked;

(d) that the duties of members of accounting staff are changed from time to time;

(e) that a satisfactory system exists for the checking of computer input and output;

(f) that the system for the control of the receipt, issue and use of stores is adequate;

(g) that the recording of the assets is up to date and correct;

(h) that returns of revenue or expenditure required by controlling officers are correctly prepared and promptly submitted.

50. Reports by internal auditors

Although internal auditors are expected to correct on the spot any errors discovered, thereby reducing the necessity for written reports, any reports which are made in writing by internal auditors will be addressed to the controlling officer of the Ministry concerned, the Secretary to the Treasury and the Auditor-General.

51. Preservation of accounting records

The following accounting records will be preserved for the periods shown:

(a) Main cash books and ledgers-10 years.

(b) Receipts of all types-10 years.

(c) Payment and Journal Vouchers-7 years.

(d) Establishment and salary records required for superannuation purposes-60 years from the date on which a pensionable officer leaves the service.

These documents will be sent to the National Archives two years after they have ceased to be in use for either audit or other purposes. Controlling officers will ensure that documents are in proper order before they are sent to the archives.

PART V

SAFES, STRONG BOXES, CASH BOXES AND SPECIE BOXES

The following instructions refer to safes, strong boxes, cash boxes, specie boxes issued for the safe custody of cash and similar forms of secure containers issued by Government, all of which shall be referred to as “safes” for the purposes of these Regulations.

53. Responsibility for obtaining safes

Controlling officers are responsible for obtaining safes from the Ministry for use in their offices and branches.

The following conditions cover the care and maintenance of safes—

(a) no work or alteration of any kind may be carried out on a safe except with the permission of the Secretary to the Treasury.

(b) small safes and strongboxes used as safes must be built into the structure of the building in which they are housed.

(c) cash boxes must be locked in a safe or a fixed container when not in use.

(d) any safe boxes in use by an officer on tour must be secured against theft by means of a chain and padlock fixed to some immovable or heavy object.

Officers are personally responsible for keys of safes in their charge.

When a safe or vault door is fitted with two or more locks, no single officer will in any circumstances hold all keys. More than one key to a safe will be issued only when there are two or more officers at the office in which the safe is installed. In the event of the departure of one of the key-holders before a relief arrives, the officer leaving the station will unlock the lock for which he holds a key and personally return this key under registered cover to the controlling officer of his Ministry.

57. Handing over of keys prohibited

A key will not be handed to a person who is not the official key-holder and a safe will not be opened except by the officer responsible for it. He must be present for the whole of the time it remains open.

Only original keys issued by the Secretary to the Treasury will be held. In no circumstances may any officer have a duplicate key made.

59. Control over duplicate keys

Except as may be otherwise authorised, all duplicate keys of safes will be held by the Secretary to the Treasury.

Inspection reports by internal auditors or other inspecting officers must include a list of safes in the offices under inspection. The serial numbers of keys must be recorded in these reports.

61. Transfer within Ministries

All transfers of safes between Departments must be notified immediately to the Ministry.

62. Transfer between Ministries

The transfer of safes between Ministries is not permitted without the prior approval of the Secretary to the Treasury.

When the key to a safe is lost—

(a) the loss will be reported immediately to the controlling officer concerned, and to the local police;

(b) the safe will be sealed and the room in which it is kept must be locked. If an exceptionally large sum is in the safe, arrangements must be made for the posting of a guard;

(c) the officer responsible for the safe custody of the key may be called upon to make good the cost of repairs and replacement of the key.

64. Private moneys in public safes

No private money or articles may be kept in a safe provided for the safe-keeping of public moneys.

A register must be kept of articles other than cash, account books and receipt forms deposited in a safe. The register must be signed by the depositing officer (other than the key- holder) when depositing or withdrawing any such article.

Officers responsible for safes must verify the contents at least once each week. The register will be initialled on each occasion of check.

Whenever cash is taken to or collected from a bank or other office, the responsibility for safe custody of the cash in transit rests with the officer charged with conveying the cash to or from the bank or other office.

PART VI

BANK ACCOUNTS AND CHEQUES

68. Bank accounts and bank signing arrangements

The opening of, or a change in, any signatory of an official bank account for any purpose requires the authority of the Secretary to the Treasury on Accounts Form 49. The purpose for which the bank account is required must be stated in a minute submitted with Accounts Form 49 by the controlling officer.

No instructions in regard to the operation of an official bank account may be issued except by the Secretary to the Treasury.

In no circumstances may public money be credited to a private bank or savings account.

Cheque books and cheque forms for use with official bank accounts will be obtained through controlling officers from the Strongroom Superintendent of the Ministry.

72. Security of unused cheques

Cheque books and cheque forms must be kept secure under lock and key when not in use. An officer will be made responsible for the custody and control of the stock of unused cheque forms. That officer will maintain a record of receipts and issues in a register (Accounts Form 103), and will ensure that all unused cheques are retained in his custody.

(1) In the event of a cheque being lost, whether the cheque is unused or has already been issued, the accounting officer must notify all local banks and head offices of all banks. In the case of the loss of a cheque which has been issued, a “stop order” must be sent to the bank on which it was drawn.

(2) Before a replacement cheque is issued for an open or crossed cheque which has been lost, or stolen from the payee, he is required to sign an indemnity in the following form:

CERTIFICATE OF INDEMNITY

In consideration of the issue to me of a replacement cheque No. ………………………….. for the sum of ………………………… in payment of ………………………….. which I have lost (or which has been stolen), I agree to indemnify the Government against any loss whatsoever in connection therewith and I agree to refund the sum of ……………………………….. in the event of the original cheque No. …………………… being negotiated.

Signed …………………………………………………………………..

NAME IN BLOCK CAPITALS ……………………………………….

Date ………………………………………………………, 20 ……….

Official Address ……………………………………………………..

……………………………………………………………………………..

……………………………………………………………………………..

……………………………………………………………………………..

The value of the replacement cheque must be debited to expenditure.

(1) Cheques drawn against official bank accounts must be signed by two or more authorised signatories except where, with the approval of the Secretary to the Treasury, cheque signing machines are used; in which case one authorised signatories will suffice.

(2) The responsibilities of signatories are laid down in Part X.

[Am by SI 69 of 1990.]

Government bank accounts must not be overdrawn, and a temporary advance must not be obtained from a bank without the prior written permission of the Secretary to the Treasury. In the event of an official account becoming overdrawn without proper authority, the officer responsible will be called upon to refund any bank charges incurred by Government as a result of the overdraft.

Cheques may, at the discretion of accounting officers, be accepted in payment of licences, fees, taxes and other payments due to Government. Before acceptance of a cheque, an officer will satisfy himself as to the identity of the person presenting the cheque and ensure that—

(a) the cheque is not post-dated or out of date;

(b) the amount in words and figures agree;

(c) the cheque is correctly signed and dated by the drawer;

(d) alterations of any kind are covered by the full signature of every signatory to the cheque.

77. Security of cheques received

Cheques received should be made payable to the Government of Zambia and crossed “Account payee only”.

When a cheque is dishonoured, the amount of the cheque will be debited to “Advances- Dishonoured and Returned Cheques” in the accounts of the Ministry concerned. Immediate action will be taken to secure prompt reimbursement of the amount owed, which must be credited to the account “Advances-Dishonoured and Returned Cheques”.

If a dishonoured cheque was originally received in payment of a licence or permit and the officer issuing such licence or permit has been unable to effect recovery within such time as is considered reasonable, but not exceeding 14 days from the date of return of such cheque, he shall declare the licence or permit to be invalid, on the grounds of non-payment of the prescribed fee, and, at the same time, he shall inform the police or other appropriate authority. In cases where it proves to be impossible to obtain reimbursement of a dishonoured cheque, the matter shall be referred to the Solicitor-General.

80. Cheques on accounts outside Zambia

Cheques, travellers’ cheques or other negotiable instruments drawn on banks outside Zambia may be paid into local bank accounts. If, for any reason, foreign cheques are not acceptable to local banks, these cheques shall be sent to the accounting unit for clearance through the Ministry. In all cases, the receiving officer shall issue a receipt for the amount paid by cheque.

81. Cashing of Government cheques

(1) At stations where there are no banking facilities, Government cheques may be exchanged for cash by accounting officers.

(2) Controlling officers may authorise in writing limited facilities for the encashment of officers’ private cheques where this is conducive to efficiency. Accounting officers will, however, act with great care as they may be called upon to make good the amount of any dishonoured cheque for which they are unable to obtain reimbursement. The privilege should be withdrawn immediately from any officer whose cheque is dishonoured.

(3) With the exception covered by sub-regulation (1) collectors of revenue or other accounting officers who receive public money may not cash cheques from public money held by them.

All officers authorised to keep official bank accounts must arrange for statements to be provided regularly by the bank. Bank statements made up to the close of business on the last day of every month will be obtained. All entries on the bank statement will be checked with the cheque backing sheet and, at the end of each month, a return will be prepared in the form prescribed in regulation 39 giving a reconciliation of the balance of the bank account with the balance shown in the cash book. This return will be submitted to the controlling officer.

Paid and cancelled cheques will be held for audit.

84. Security of cheques in payment for goods supplied on Local Purchase Orders

All cheques drawn in payment for goods supplied on Local Purchase Orders should be crossed “Account payee only”. The only exception to this rule is in the case of a payee known to have no banking account. Stamps showing this restrictive crossing will be supplied on application by the Government Printer.

PART VII

RECEIPT FORMS

85. Definition of “receipt form”

The term “receipt form” includes all receipts, licences, permits, certificates, discs or tokens used in the collection of revenue or other moneys.

(1) All licences, permits, certificates, discs, tokens and other documents for which payments are received will be issued on or with the prescribed forms.

(2) A “General Receipt” (Accounts Form 40) will be used in cases where a special receipt form is not prescribed.

(1) Supplies of receipt forms will be obtained only from the Strongroom Superintendent of the Ministry, by the submission of a requisition. In no circumstances will any officer make arrangements for the printing or alteration of receipt forms other than through the Secretary to the Treasury.

(2) Receipt forms will be issued only to Government accounting officers or to local authorities.

88. Auditor-General to be informed

The Auditor-General will be informed of all issues and transfers of receipt forms.

89. Checking receipts received

All receipt forms must be checked immediately they are received to ensure that they are complete and correctly numbered. Any forms which are defective must be returned to the Strongroom Superintendent without delay. The Advice of Issue of Licences, Revenue Stamps and Receipt Books (Accounts Form 45) must be receipted and returned immediately to the Strongroom Superintendent with a report of any discrepancies, which must be copied to the Auditor-General and the controlling officer.

Every officer required to hold receipt forms will keep a Register (Accounts Form 103) in which the receipt and issue of all receipts forms must be promptly entered. These registers will be obtained from the Government Printer.

Books of receipt forms will normally not be transferred from one holder to another. If in an emergency such a transfer becomes necessary, the transfer must be reported immediately to the Auditor-General and the controlling officer.

Receipt forms will be used in consecutive order, within the sequence of numbers of receipts held by one officer.

93. Unused and surplus receipts

Surplus stocks of completely unused receipt books which are not obsolete should be listed and returned by registered parcel post to the Strongroom Superintendent. Copies of lists will be sent to the Auditor-General and to the controlling officer.

94. Destruction of obsolete receipts

Complete unused books of obsolete receipts will be destroyed at the office in which they are held. The destruction of the receipt books will be carried out in the presence of the accounting officer in charge, and another officer who will check that the unused receipt books are complete, and that all receipts are in fact unused. Certificates of destruction, listing the serial numbers of all receipt forms destroyed, must be signed by both officers. The original of the certificate of destruction will be filed by the officer responsible for the custody of the forms and copies must be sent to the Auditor-General and the controlling officer.

95. Recording of destruction of obsolete forms

Whenever surplus stocks of receipt books are returned to the Strongroom Superintendent or whenever obsolete forms are destroyed, the fact should be recorded in the Register (Form 103).

96. Reporting of loss of or damage to receipt forms

If a book of receipts or part of a book is lost or damaged, the holder will report immediately to his controlling officer with copies to the Auditor-General and to the Secretary to the Treasury.

97. Monthly check of unused receipt forms

A check of unused receipt forms will be carried out at least once a month by the holder, who must record in the Register the date of check and sign the entry.

98. Handing over certificates to record receipt forms

When one officer hands over to another, handing/taking over certificates must be signed by both officers for receipt forms. The officer taking over should sign immediately below the last entry in the Register.

99. Notice to public about official receipts

A printed notice obtainable from the Ministry must be displayed in all offices where revenue of any type is received, to bring to the attention of the public the need for them to obtain an official receipt for every payment made by them.

Receipt forms must be completed either in ink or in indelible pencil. Counterfoils will contain exactly the same details as appear on the original receipt form. They should be date-stamped at the time of issue and will not be altered in any way.

If a wrong entry is made on a receipt, the form must be cancelled and dealt with in the manner prescribed in regulation 102.

102. Method of cancelling receipts

When a receipt is cancelled, the original and all the copies must be cancelled, and the cancellation signed by the holder of the book. The original receipt will be kept in the receipt book. The duplicate will be included with other duplicate receipts which accompany the Revenue Cash Book.

103. Office of issue of receipts

Every receipt form and counterfoil will be printed or stamped with the official stamp of the office of issue and will be signed by the issuing officer.

Officers receiving payments from collectors of revenue must ensure that numbers of receipt forms issued by the collectors run consecutively. If no satisfactory explanation is forthcoming for any missing forms, the matter will be reported without delay to the controlling officer of the Ministry concerned.

105. Free issue of receipt form

When a free issue is made of a receipt form for which a fee would normally be payable, the following certificate will be endorsed by the issuing officer on the form and its counterfoil or copies:

“I certify that this (licence) is issued free under the provisions of

……………………………………………………………………………..

……………………………………………………………………………..”

In no circumstances may a duplicate of a licence be issued unless approval for such issue is specifically provided in any Law or regulation.

107. Certified copies of receipt forms

If a certified copy of a receipt form is required, this will be made on plain paper and headed “certified copy”. In no circumstances will another receipt form be used as a copy for an original receipt previously issued.

108. Transfer and destruction of receipt forms

It is strictly forbidden to transfer used receipt forms from one accounting unit to another, or to destroy the counterfoils and copies of used receipt forms until after they have been examined by the Auditor-General.

PART VIII

RECEIPT OF REVENUE

109. Private use of revenue prohibited

Officers are not permitted to use public revenue, temporarily or otherwise, for any private purpose whatsoever.

A receipt form must always be issued by the receiving officer whenever a sum of public money is received.

All receipts must be vouched for on the form prescribed by statute or regulation.

The notes and coins issued by the Bank of Zambia constitute legal tender in the Republic. No other currencies may be accepted without the specific authority of the Secretary to the Treasury.

Applications must be made to the Secretary to the Treasury for general permission to accept specified foreign currency notes, travellers’ cheques or cheques drawn on foreign banks at current rates of exchange.

114. Remittance of foreign currency

Foreign currencies which are not acceptable to local banks will be remitted to the accounting unit for onward transmission to the Ministry, and may not, under any circumstances, be paid to a commercial bank or exchanged for Zambian currency.

115. Classification of revenue

All revenue will be brought to account under the appropriate sub-head of the revenue estimates.

Collectors of revenue will keep a cash book which must be written up daily. Accounts Form 47B provides for the collection of revenue under four headings but where more columns are required Accounts Form 47A will be used.

117. Bringing revenue to account

Collectors of revenue are required to bring to account daily the whole amount of their collections. Controlling officers will institute checks to ensure that this is done.

118. Deposits to the Main Account

The following facilities will be used to enable deposits to be made to the Main Banking Account with the Bank of Zambia. Revenue will be deposited—

(a) where daily banking facilities exist, either directly with the Bank of Zambia or indirectly by mail transfer through a commercial bank;

(b) where a banking agency or mobile banking service exists, by mail transfer through the agency to the Bank of Zambia on every opening or visit;

(c) where no banking facilities exist, by obtaining a commission-free money order for the cash received. This money order and any cheques will be sent by registered post to the Bank of Zambia for deposit to the Government’s Main Account.

If it is found that a collector of revenue has a surplus of cash, this must be brought to account and credited to the “Miscellaneous” sub-head of the revenue estimates under “Finance” (“Fees of Court”, etc.).

120. Revenue collectors not to open mail

An officer who is responsible for issuing receipts must not be concerned in opening mail or keep a register of incoming remittances.

Receipts in respect of the recovery of overpayments or erroneous payments should be credited to the vote from which the payment was made, unless the payment was made in a previous financial year, in which case the receipt should be credited to the item provided in the revenue estimates “Finance-Miscellaneous” (under “Fees of Court”, etc.). Recoveries of overpayments or erroneous payments made from the Capital Fund should be credited to the Capital sub-head from which the payment was made, unless that sub-head has been closed, in which case the credit should be made to the “Other Miscellaneous Receipts” head of Capital Revenue.

122. Revenue not to be credited to suspense account

Revenue collected in any one year shall not be credited to a deposit account with the object of transferring it to revenue in the following year.

Revenue may be abandoned only with the approval of the Secretary to the Treasury. An application for this authority must give the sum of the revenue, the date on which it was due, the action taken to collect it and the reasons why it was not possible to collect it. A copy of the application will be forwarded to the Auditor-General. Should the Secretary to the Treasury authorise the abandonment of the revenue, a copy of his authority will be forwarded to the Auditor-General.

PART IX

REFUNDS OF REVENUE

A controlling officer may authorise a refund of revenue only if—

(a) approval for a refund of revenue is made under legislation or other authority for which his Ministry is responsible;

(b) a refund must in equity be made, e.g. where a tax or a fee has been paid twice in error.

Applications to the Ministry for authority to refund stamp duty will be supported, whenever possible, by the stamped documents in respect of which the refunds are sought.

Payment vouchers relating to refunds of revenue must quote the authority for the refund. The number of the receipt on which the revenue was originally collected will be quoted on the payment voucher. The original of the receipt should be attached to the payment voucher.

Court fees and fines may be refunded by the Registrar of the High Court or by the Judge or magistrate of the Court to which the fees or fines were paid.

128. Classification of refunds

(1) Refunds of revenue for the Department of Taxes and the Department of Customs and excise shall be debited to the sub-head of revenue to which the amount to be refunded was originally credited.

(2) All other refunds of revenue shall be charged against the expenditure vote “Finance Recurrent Department Charges: Refunds of Revenue”. No payment shall be charged against this vote without prior authority of the Secretary to the Treasury.

[Am by SI 42 of 1976.]

PART X

CONTROL OF EXPENDITURE AND PAYMENTS

As the Approved Estimates of Recurrent and Capital Expenditure are not in themselves authority to spend funds, any payments which are charged to expenditure provided for in the estimates may only be made by warrant-holders who are officers holding one of the following authorities—

(a) A Treasury Authority or warrant issued by the Secretary to the Treasury.

(b) A warrant issued by a controlling officer to a warrant-holder in his Ministry.

(c) A sub-warrant issued by a warrant-holder.

All payment vouchers must contain the authority against which expenditure is incurred, e.g. warrant number, or Law or special minute.

There is no necessity to keep a commitment ledger. A box-file will be used instead as follows—

(a) one or more box-files will be kept for the purpose of filing the triplicate copy of each Local Purchase Order, the “number 3” copy of each stores requisition, and a copy of each indent, contract, or other record of commitment;

(b) once the order has been paid, the relevant Local Purchase Order, etc., will be removed from the commitment file to its final storage place. The commitment file should be kept at the office where payment is made but, if this is not appropriate, it should be kept at the ordering office and the copy order removed from the file at the time an approved payment voucher is dispatched to the paying office;

(c) a part-payment will be recorded as such on the face of the relevant Local Purchase Order, indent, etc.;

(d) a manual or machine list will be prepared at each month-end, showing the total value outstanding against each item of a sub-head. When added to the expenditure to date, the totals will be compared with the “Amount Authorised” column of the estimates.

132. Payments on behalf of other Ministries

No payments will be made against the vote of another Ministry without an authority, usually in the form of a warrant or sub-warrant issued by that Ministry. This prohibition applies to Zambia Missions abroad which will not make payments to officers without specific authority in writing from the Ministry concerned.

The date of payment will govern the date of record of a transaction in the accounts, unless specific authority to the contrary is given by the Secretary to the Treasury. Unexpended portions of a vote during the year may not be drawn and placed on deposit for the purpose of setting aside funds as a reserve to meet payments in the next financial year. On the other hand, expenditure properly chargeable to the accounts of a financial year will, so far as possible, be made within that year and will not be deferred for the purpose of avoiding an excess on the authorised provision for the year in which authority should have been obtained by Supplementary Provision.

(1) All payments must be vouched for on one of the following forms:

Accounts Form 2: A wages payment voucher.

Accounts Form 5: A general payment voucher.

Accounts Form 44: A claim and payment voucher used for travelling on duty including mileage and subsistence.

(2) Accounts Form 69 which provides payees with details of the payments should be used in conjunction with Accounts Form 5.

135. Details on payment vouchers

All vouchers must be complete and all details must be filled in, including coding allocations, dates, numbers, quantities, rates, distances and authorities.

Vouchers will be typewritten or made out in ink or indelible pencil. All copies must be legible.

The original of a payment voucher will be signed by a controlling officer, a warrant-holder or by any officer authorised by them to sign on their behalf. The name of the officer signing and his designation will be printed below his signature. Copies will be initialled by the signing officer or stamped with his name stamp.

138. Panel of signing officers

A list of accounting or other officers authorised in writing to sign vouchers on behalf of warrant-holders will be sent by controlling officers to the Auditor-General and amended from time to time. Normally, these signing officers should not be below “executive” rank.

139. Responsibilities of officers signing -vouchers

The officer signing a voucher or document certifies the accuracy and validity of the payment. He must therefore ensure that—

(a) all deductions due to be made from salaries or wages have in fact been made;

(b) the goods have been supplied or the services provided as certified by the receiving officer;

(c) the prices charged are either according to contract or approved rates, or are fair and reasonable according to current local rates;

(d) the payment is covered by proper authority and is a proper charge to public funds;

(e) the calculations are correct;

(f) the persons named as payees are those entitled to receive payment;

(g) the voucher is properly allocated to a head, sub-head and item;

(h) payment of the amount stated on the voucher will not cause an excess over the amount allocated to him.

Officers signing vouchers which relate to payments which are recoverable are responsible for ensuring that proper arrangements exist for the recoveries to be made.

141. Suppliers’ invoices to be attached

Vouchers relating to purchases must be supported by the suppliers’ invoices. Payment will not be made on statements of account only. On no account will requisitions for local supplies be issued in arrear if goods have already been supplied. In such cases, the responsible officer will certify the voucher giving reasons for the failure to issue a requisition.

Should an original invoice be mislaid, a duplicate will be obtained from the supplier. The duplicate will be clearly marked “Copy Invoice”. A certificate that payment has not previously been made will be recorded on the voucher by the officer making the payment, after he has satisfied himself that payment of the account has not in fact been made.

143. Mislaid requisition forms

In no circumstances will a duplicate requisition form be issued if an original has been mislaid. Payment will be made against the supplier’s copy invoice which will be endorsed with the serial number of the requisition form against which the supply of goods or services was made, and the certificate required by regulation 142 will be recorded on the payment voucher.

144. Payments on incorrect certificates

In the event of any unauthorised payment being made in consequence of an incorrect certificate on a voucher, the certifying officer may be held responsible and may be surcharged with the amount involved.

(1) With the exceptions stated in sub-regulation (2), the normal method of payment to payees outside Zambia will be through the Secretary to the Treasury. Ministries with inter-departmental clearance (IDC) facilities will forward to the Secretary to the Treasury the following documents duly completed—

(a) Accounts Form 5.

(b) Accounts Form 69.

(c) An appropriate IDC.

Originators without IDC facilities will substitute a cheque for an IDC in paragraph (c).

(2) Payments by missions abroad for the maintenance and staff salaries of those missions are made direct by them.

Payments will be made by cheque or cash, whichever is the more economical and convenient. If made by cheque, the cheque will be made payable to those to whom payment is due. Each cheque must be crossed, except in the following circumstances—

(a) Open cheques may be issued in the case of standing imprests and for the net total of vouchers in respect of wages to be paid in cash to junior employees and labourers. These cheques will be made payable to the order of the title of the post held by the officer responsible for drawing the cash and paying the wages. For the guidance of banks and Government offices at which cheques will be cashed, the name of the responsible officer will be added in brackets.

(b) Open cheques payable to the order of the payee may be issued for personal imprests and, on request, for salaries, wages and other personal payments due to Government employees.

When an open cheque is issued, a receipt or acknowledgement of the cheque will be obtained from the payee before the cheque is handed over or, if the cheque is sent by mail, it will be sent by registered mail and the number of the registered slip recorded on the payment voucher.

148. Responsibilities of cheque signatories

Provided that there is no loss of discount for prompt payment, accounts for the same supplier may be grouped and paid at least once every month. Should any discount be lost owing to delay in the passing of accounts for payment, the officer responsible may be called upon to refund the amount to Government.

All signatories of cheques are responsible, when signing, for ensuring—

(a) that original documents (invoices, salary sheets, claim forms, etc.) are attached;

(b) that the original documents are all stamped “Paid” by means of a special stamp obtainable from the Ministry, and that the cheque number is correctly shown within the “Paid” stamp;

(c) that the relevant Payment Voucher (Accounts Form 5) is fully and properly completed;

(d) that the cheques are correctly made out in every respect.

150. Delivery of cash or cheques

Only in the following circumstances may payments be made other than to the persons or firms to whom payment is due—

(a) On the written authority of the person or firm to whom the payment is due or on the production of a power of attorney or letter of administration.

(b) In cases where the timely payment of wages to an employee is impracticable and delay would cause hardship, a paying officer may on his own responsibility make payment to a third party who will give a receipt for the payment. The paying officer will also satisfy himself that the payee receives the payment due to him.

(c) In cases where payment is made to a duly appointed receiver, an official receiver, a trustee in bankruptcy or to a third person under a Court order.

Paying officers and officers who are witnesses to a payment will satisfy themselves that the person claiming the payment is in fact the person authorised to receive the money. If necessary, they will require the production of a National Registration Card.

152. Daily accounting for payments

All payments will be entered into the books of account on the day the payments are made.

(1) Fares and transport charges for travel or the consignment of stores will be met by the issue of the following warrants or requisitions:

Rail – Rail warrant:

Accounts Form 29 (Passengers); Accounts Form 30 (Goods).

Road-Road transport requisition; Accounts Form 33 (b).

Air-Requisition for Official Passage by Air:

Accounts Form 33 (c).

(2) These warrants and requisitions must be fully and accurately completed, particularly with regard to the following details when applicable—

(a) The purpose of the journey must be stated and it is not sufficient to use only the words “on duty”

(b) The ages of all children must be entered.

(c) Whenever a concession fare can be claimed, completed concession vouchers must be attached to the warrant when it is presented for the issue of a ticket.

(d) The conditions of service on which the officer travelling is employed must be clearly endorsed on the warrant/requisition.

(e) The actual weight of baggage to be carried must be entered on a warrant/requisition. It is not sufficient merely to indicate on the warrant/requisition the maximum amount of baggage which can be transported at Government’s expense.

(f) Where it is stated in General Orders, or any other regulation, that an officer may transport a limited amount of baggage by passenger train and the remainder by goods train, separate warrants will be issued. The number of the warrant issued for the transport of personal effects by goods train must be entered in the appropriate space on the warrant issued for the effects to be carried by passenger train.

154. Responsibility of officers signing warrants, etc.

Officers signing warrants, requisitions and stores orders are approving the expenditure of public funds and they will be responsible, therefore, for seeing that the proper authority exists for the expenditure thus incurred. They will also be responsible for ensuring, in the case of passenger fares, that officers are entitled to the free fare and that all appropriate concessions are claimed. Any excess expenditure incurred as a result of the failure to observe regulations may be surcharged against the officer who signed the warrant, requisition or stores order.

Payments which are extraordinary in that they are not covered by normal regulations or procedures, e.g. compensation for loss of or damage to private property, require the prior approval of the Secretary to the Treasury.

156. Custody of original documents

(1) Payment vouchers with supporting documents, and any other forms which support a charge entered in the accounts, will be carefully filed, secured against loss, and be readily available for audit.

(2) Access to the documents should be restricted to those officers authorised by the accounting officer to make reference to them. In no circumstances will the documents be removed from the files in which they are kept.

If a payment voucher is lost a properly certified duplicate will be obtained. If this is not possible, the expenditure will be treated as unvouched and written application must be made immediately to the Secretary to the Treasury, with a copy to the Auditor-General, for authority for the payment to stand as a charge to public funds. The application will provide the following details—

(a) the number and date of the voucher;

(b) the amount of the payment;

(c) the allocation of the charges;

(d) the name of the payee;

(e) the nature of the payment;

(f) an explanation as to why the voucher was lost;

(g) whether the cheque issued was crossed or open;

(h) whether the cheque was endorsed or receipted by the payee; and in respect of purchases:

(i) the purchase order number and date;

(j) the invoice number and date;

(k) a certificate that the goods have been received and brought on charge.

The controlling officer is required to certify that, after making a thorough check, he has been satisfied that the payment is authentic and that the payee has received the payment which the original voucher covered.

PART XI

PAYMENT OF SALARIES AND WAGES

Salaries and monthly wages will be paid on the last working day of each month or according to any staggered dates which the Secretary to the Treasury may from time to time approve.

Salaries are payable in monthly instalments calculated at one-twelfth of the annual rate. Salaries for a part of any month will be calculated in proportion to the number of days in that particular month, e.g. salary for eight days in April would be eight-thirtieths of the monthly rate.

160. Salaries and wages not to be paid in advance

Except as provided for in General Order 205, an officer will not be granted an advance of salary or wages.

161. Adjustment of salary or other moneys due to death, etc.

Any contingency which is likely to affect an officer’s salary (e.g. his death, suspension or dismissal) will be notified immediately by the controlling officer to the senior officer in charge of salaries in the Ministry. The latter will then be responsible for ensuring that timely and correct adjustments are made to the officer’s salary, pension or gratuity.

162. Salaries of convicted officers

Any balance of salary or other moneys due to an officer who has been convicted of misappropriation of Government funds or theft of Government property or who has been dismissed, leaving sums owing to Government (including losses of cash or stores which are under investigation), may not be paid without the authority of the Secretary to the Treasury.

163. Method of payment and deductions: Divisions I and II

A separate salary record card for each Division I and II officer in the Service will be kept by the Ministry. The salaries of Division I and II officers are paid by the Ministry on the basis of information supplied by the Secretary to the Treasury (Establishments) and the controlling officer of the Ministry in which those officers are serving. Officers will make arrangements regarding the method of payment, and the permissible voluntary deductions, through their controlling officers.

Payment of salary may be made direct to the credit of an officer’s account at any commercial bank or building society in Zambia, or by cheque. Payment of the net amount due, after statutory and permissible deductions have been made, will be made in one sum; there will not be a part-payment to the credit of a bank account with the balance paid by cheque or otherwise.

165. Dispatch of salary cheques

All open cheques will be dispatched under registered cover or delivered against personal signatures. Salary cheques will be forwarded, in bulk, from the Ministry to controlling officers. A signature, followed by the signing officer’s printed name and rank, will be required for the total number of cheques received. These will be listed by serial numbers. Controlling officers will be responsible for the distribution of these cheques and for obtaining the payees’ signatures in acknowledgement of receipt of the cheques. When cheques are dispatched to officers in charge of out-stations, for redistribution, Distribution Lists (Accounts Form 139) will be used and addressees will be responsible for obtaining the payees’ signatures. The lists, when completed, will be returned immediately to the sender who will retain them as a permanent record. If it is necessary to post the cheque direct to the actual payee, the remittance will be posted under registered cover and the registration number will be inserted against the entry in the Distribution List.

166. Deduction of rent for official quarters

Rent for official quarters will be deducted from salary at the full rate unless exemption or reduction has been claimed and approved. The responsibility for claiming reduced rent or exemption, including exemption during periods of vacation leave, rests with the officer concerned. Claims will be made direct to the Ministry with a copy to the officer’s controlling officer. Accounts Form 133, 134 or 135, as appropriate, will be used for this purpose. Recovery of rent in respect of non-civil servants will be the responsibility of the employing Ministry.

167. Payment scales and rates: officers other than those in Divisions I and II

Salaries and wages of employees other than those in Divisions I and II of the Civil Service will be paid by the Ministries in which they are employed, in accordance with scales and rates laid down by the Permanent Secretary (Establishments).

168. Gross salary and deductions to be charged

All authorised deductions will be entered on the payment vouchers in the appropriate column against the name of each employee concerned. The gross emoluments will be charged against the relevant sub-head and deductions will be credited to the appropriate account.